Monthly Budget That Actually Works Last Friday, I found myself staring at my bank account with that all-too-familiar sinking feeling. Somehow, with ten days left in the month, I was already running dangerously low on funds. Again. Sound familiar? Your company is good if you’re nodding right now. I’ve spent years perfecting the art of creating budgets that look beautiful on Sunday night but completely fall apart by Tuesday afternoon. But after countless false starts and financial face-plants, I’ve finally cracked the code on creating a budget that doesn’t just look good—it actually works. So you don’t have to learn the hard way, let me share what I have learned the hard way.

Why Most Budgets Fail (I Should Know, I’ve Failed at Plenty)

Monthly Budget That Actually Works Let’s be real: most budgets crash and burn because they’re about as realistic as my plan to wake up at 5 AM for yoga every day. For years, I created beautiful spreadsheets that left zero room for, well, life. No provisions for when my car decided to throw a check engine light, or when my best friend announced a destination wedding, or even for the psychological reality that sometimes, after a week from hell, a takeout pizza feels less like a luxury and more like emergency self-care.

The lightbulb moment came when I realized successful budgeting isn’t about following some financial guru’s perfect template—it’s about creating a money system that accounts for my actual life, complete with its messiness, spontaneity, and yes, occasional retail therapy. Your budget needs to work with your real income, your real expenses, your real goals, and (this is the big one) your real habits and values.

Step 1: Figure Out Where Your Money Is Actually Going (Brace Yourself)

Before diving into budget creation, you need to face the sometimes uncomfortable truth of where your money is really going. I still remember the pit in my stomach when I realized I was spending more on coffee shops each month than on my utilities. Ouch.

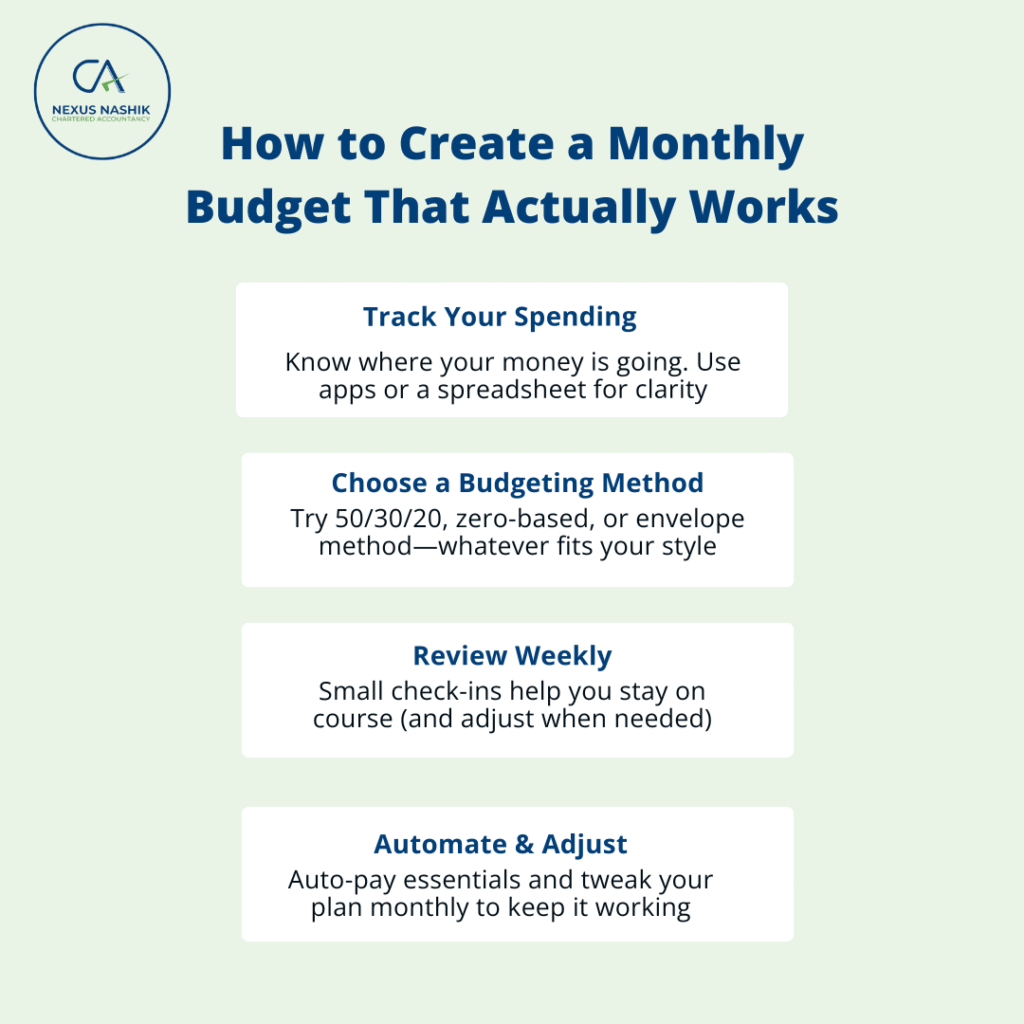

Track Every Single Penny (Yes, Even That $3 Vending Machine Snack)

For the next 30 days, channel your inner detective and document every expense. Choose a tracking method that won’t make you pull your hair out:

- Budgeting apps like Mint, YNAB, or Personal Capital if you’re tech-friendly (I’m a YNAB devotee myself)

- A simple spreadsheet if you love Excel (or are too stubborn to pay for an app—I’ve been there)

- Going old-school with a small notebook you carry everywhere

- Bank statements, though these miss the cash transactions (like that $20 that mysteriously vanishes from your wallet every weekend)

As you’re tracking, sort your spending into these buckets:

- The non-negotiables (rent/mortgage, loan payments, insurance—the stuff that keeps a roof over your head and collectors away from your door)

- The necessary but flexible stuff (groceries, utilities, gas—you need them, but you have some control over how much you spend)

- The “where did my money go?” category (dining out, Target runs where you went in for toothpaste and left with $75 worth of things you didn’t know you “needed,” subscription services you forgot you signed up for)

Warning: This exercise will probably deliver some hard truths. When I first did this, I discovered I was spending an embarrassing amount on food delivery services—enough to fund a decent vacation each year. That $15 delivery fee here and there adds up faster than you’d think!

Step 2: Calculate Your Income

Next, determine your total monthly income. Include:

- Net salary (after tax)

- Side hustle earnings

- Passive income (investments, rental properties)

- Any other regular income sources

Depending on your income, calculate your average monthly earnings from the past 6 to 12 months. Make sure you set aside money during high-income months so that you will be able to support yourself during the lean months.

Step 3: Define Your Financial Goals

Effective budgeting isn’t just about controlling spending—it’s about intentionally allocating resources toward what matters most to you. Take time to identify:

Short-term goals (within 1 year):

- Building an emergency fund (3-6 months of essential expenses)

- Paying off high-interest debt

- Saving for an upcoming vacation Medium-term goals (1-5 years):

- Putting together a down payment for a house

- Funding a career change or education

- Replacing your vehicle Long-term goals (5+ years):

- Retirement planning

- Children’s education funds

- Achieving financial independence

Prioritize these goals based on importance and timeline. Each should have a specific target amount and deadline to make them actionable.

Step 4: Choose Your Budgeting Method

There’s no perfect budgeting method—the best approach is one you’ll actually use consistently. Here are popular methods to consider:

50/30/20 Budget

- 50% for needs (housing, food, transportation, utilities)

- 30% for wants (dining out, entertainment, hobbies)

- 20% for savings and debt repayment

This straightforward approach works well for beginning budgeters with relatively stable incomes and reasonable debt loads.

Zero-Based Budget

With this method, you give every dollar a job, allocating your entire income across expense categories, savings, and debt payments until you reach zero. This comprehensive approach requires more maintenance but provides maximum control.

Pay Yourself First

Automatically direct a predetermined percentage of income to savings and investments before budgeting the remainder for living expenses. This method prioritizes long-term financial health and simplifies day-to-day money management.

Envelope System

Create physical or digital envelopes for different spending categories. Spending in an envelope is stopped when it is empty until the next budget period. This tangible approach helps over spenders develop better habits.

Step 5: Create Your Budget Framework

Now it’s time to build your actual budget. Using insights from your expense tracking and selected budgeting method:

- List all income sources and their amounts

- List all fixed expenses with exact amounts

- Determine variable necessities based on historical spending patterns

- Designate money for savings goals and debt repayment

- Distribute remaining funds across discretionary categories

Remember to include often-forgotten expenses such as:

- Annual memberships and subscriptions

- Seasonal costs (holiday gifts, back-to-school shopping)

- Vehicle maintenance and registration

- Medical copays and deductibles

- Home repairs and maintenance Step 6: Build in Flexibility with a Buffer Category

One common reason budgets fail is their inability to handle unexpected expenses. Create a small “buffer” or “miscellaneous” category (about 5% of your budget) to cover unforeseen costs without derailing your entire plan.

This category differs from your emergency fund, which should only be tapped for true emergencies like job loss or major medical expenses. The buffer handles smaller surprises like a last-minute gift or minor car repair.

Step 7: Automate What You Can

Reduce the mental load of budgeting by automating regular financial tasks:

- Set up direct deposit for paychecks

- Schedule automatic transfers to savings accounts

- Use automatic bill pay for fixed expenses

- Establish automatic investments for retirement accounts

Automation ensures consistent progress toward financial goals and reduces the risk of late payments or forgotten transfers.

Step 8: Implement Regular Budget Reviews

A successful budget evolves with your life circumstances. Schedule regular reviews:

Weekly mini-reviews (15 minutes):

- Check account balances

- Review upcoming bills

- Adjust for any immediate concerns Monthly comprehensive reviews (1 hour):

- Compare actual spending to budgeted amounts

- Identify categories needing adjustment

- Celebrate wins and progress toward goals Quarterly strategic reviews (2 hours):

- Assess progress toward larger financial goals

- Make seasonal adjustments

- Reevaluate priorities if needed Annual budget overhaul (half-day):

- Reflect on the past year’s financial journey

- Update income projections and fixed expenses

- Revise financial goals as needed

- Plan for major upcoming expenses

- Step 9: Use Tools That Support Your Budgeting Style

The right tools can dramatically simplify budget management:

For the tech-savvy:

- Comprehensive apps like YNAB, Mint, or Personal Capital

- Spreadsheet templates with built-in calculations

- Banking apps with spending analysis features For the tactile budgeter:

- Cash envelopes for variable spending

- Budget binders with printed worksheets

- Visual trackers for savings goals

For the minimalist:

- Simple spreadsheets with essential categories only

- Basic tracking apps like Good budget or Every Dollar

- Automated savings with minimal manual tracking

Step 10: Develop Healthy Money Habits

Even the most meticulously designed budget won’t work without supportive financial habits:

Practice mindful spending

Before making purchases, especially unplanned ones, pause and ask whether this expense aligns with your values and goals.

Implement a waiting period

For non-essential purchases over a certain amount (say $50 or $100), wait 24-48 hours before buying. This reduces impulse spending.

Find accountability

Share your financial goals with a trusted friend, join a money management group, or work with a financial coach who can provide support and perspective.

Celebrate milestones

Acknowledge your progress with appropriate rewards that don’t derail your budget.

Common Budgeting Challenges and Solutions

Challenge: Irregular Income

Solution: Create a “baseline budget” covering essential expenses, then develop a prioritized list of where additional money goes in higher-income months. Maintain a larger emergency fund to cover lean periods.

Challenge: Shared Finances in Relationships

Solution: Schedule regular money meetings with your partner, maintain some financial independence with personal spending allowances, and focus discussions on shared goals rather than individual spending habits.

Challenge: Budget Fatigue

Solution: Simplify your system, build in small rewards, and remember your “why”—the meaningful goals your budget helps you achieve.

Challenge: Unexpected Expenses

Solution: Beyond your emergency fund, create sinking funds for predictable irregular expenses like car repairs, medical costs, and home maintenance.

The Real Bottom Line: Progress Over Perfection (Because We’re Human, Not Spreadsheets)

Let me share something I wish someone had told me years ago: You will mess up your budget. Repeatedly. There will be months when unexpected expenses blindside you, when willpower fails, or when life simply happens. I once blew my carefully crafted budget three days after creating it because my car needed emergency repairs the same week my best friend was going through a breakup that required emergency ice cream and wine.

The secret isn’t never failing—it’s getting back up after each financial stumble without beating yourself up. Budgeting is like learning to ride a bike; those training wheels didn’t come off after one perfect loop around the driveway.

Your budget will—and should—evolve as your life changes. The ultra-frugal plan that worked during your debt payoff crusade might feel suffocating once you’ve reached that goal. The carefree spending of your higher-income years might need tightening when you decide to go back to school. Give yourself permission to adjust and grow.

What I’ve discovered after years of financial trial and error is that budgeting eventually transforms from a dreaded chore into something empowering. It becomes less about what you can’t have and more about consciously choosing what matters most to you. My coffee shop visits haven’t disappeared from my budget—I’ve just made room for them by deciding other things matter less to my happiness.

Start exactly where you are today. Use whatever tools you have available. Take one small step, then another. Your journey to financial control isn’t about reaching perfection—it’s about building a life where your money finally serves your dreams instead of your money controlling you.